by Kyle Johnson

My distaste for modern economics ratchets in only one direction.

If you’ve followed US labor market statistics over the past year or so, you’ve probably encountered the work of Claudia Sahm—a PhD economist who’s worked at the Federal Reserve and the Brookings Institute.

I’m unimpressed. Here’s why.

The “Sahm” Rule

First things first. Here’s the “Sahm” Rule as she tells it in a Bloomberg article:

“Before the pandemic, I developed a highly accurate recession indicator, later named the Sahm rule ….

“The Sahm rule is simple. If the three-month average of the unemployment rate (the monthly rate often bounces too much) is half a percentage point or more above its low in the prior 12 months, the economy is in a recession.”

Simple enough.

Sahm boasts, “I created the Sahm rule, and I take full responsibility for it.” After reading Mike “Mish” Shedlock’s blog, I find that statement rather concerning. Shedlock has multiple posts discussing the work of Ed McKelvey (Goldman Sachs). Published in the Wall Street Journal on January 4, 2008, an article titled “Unemployment Rate Crosses Recession Threshold” reads:

Economists at Goldman Sachs say once the three-month average of the unemployment rate has risen 0.3 percentage points, the economy has always either been in, or about to enter, a recession.

Well, that sounds awfully familiar. The WSJ goes on to mention McKelvey by name.

You can read Sahm’s thesis published in 2019 on the Brookings Institute website. Try as you might, you won’t find any mention of Ed McKelvey, Goldman Sachs, or the Wall Street Journal. In fact, I cannot find a single instance of Sahm mentioning McKelvey anywhere.

Not a good look.

“Sahm” Rule Triggered?

Ironically, Sahm was thrust into the spotlight in November 2023 when the three-month average crossed 0.3 (McKelvey’s threshold). Without mentioning him, Sahm reassured everyone there was nothing to fear as her 0.5 threshold had not been breached.

In a Bloomberg piece, Sahm cites economist Julia Coronado, who argued that the rising supply of workers is good for the labor market even if it shows up in somewhat higher unemployment statistics. Sahm reasoned, “If that’s the case, recession indicators based on unemployment rate, like the Sahm rule, may not be accurate in this time.”

Did you catch that?

If that’s the case.

Sahm’s 0.5 threshold was breached in August 2024. She took to Bloomberg to explain that the “Sahm” Rule worked historically when the unemployment rate rose due to weakening demand for workers. But this time, unemployment rose primarily due to an increase in the supply of workers (immigrants). A substantial difference, she tells us, but one “her” rule did not account for. She insists we must make allowances and concede as fact that new entrants to the labor force take longer to find work.

I find it humorous that she made these arguments in a piece titled “My Recession Rule Was Meant to Be Broken.” In November 2023, Sahm wasn’t committed to a supply shock causing a false positive (remember, she said “if that’s the case”). Her 2019 thesis makes no mention of this dynamic either. Did this PhD economist “create” a rule about the labor market without anticipating changes in supply?

Being ex post facto is just one of many problems with Sahm’s flippant explanation. She also ignores what is likely the single greatest shock to the labor supply in US (if not world) history—the end of World War II.

Many official statistics show a depression beginning in 1946. But scholars like Richard K. Vedder, Lowell Gallaway, and Robert Higgs went through data and found that it was a time of economic prosperity and rapid free-market adaptation. They show that claims of recession rely on faulty statistics.

From 1945 to 1946, statistics from Department of Commerce show that real GNP shrank 12–19%. But economist Simon Kuznets highlights the difficulty in valuing and comparing war and non-war sectors. After adjusting the data, he estimates real GNP rose anywhere from 8–16%.

The end of the war sent many economists into a panic. More than four million soldiers returned to US soil before 1946. They saw mass unemployment on the horizon.

Business Week predicted that GNP would be 20% lower than 1944 levels, and unemployment would peak closer to nine million than eight million (about 14% of the projected civilian labor force). In December 1945, Robert Nathan predicted six million would be unemployed by spring (about a 10% unemployment rate).

The labor market had to deal with much more than just returning soldiers. Higgs estimates that in fiscal year 1940, a staggering 40% of the labor force was part of what he called the labor force “residuum”—people entirely dedicated to the war effort (i.e., not producing goods and services for civilian consumption). In this figure, he includes unemployed civilians, members of the armed forces, civilian employees of the armed forces, and employees in the military supply industry. This figure dropped from 40% in 1940 to 11.5% in 1946.

A Bureau of Labor Statistics (BLS) conception puts civilian unemployment at just 2.6% in 1946, up from 1.3% the year prior.

Millions of soldiers returned to the labor force, and millions more quickly switched from producing goods for the war effort to producing goods for civilian consumption. Economist Thomas DiLorenzo notes that private-sector production increased by 33% in 1946 alone, as capital investment increased for the first time in nearly two decades. Kuznets and economist John Kendrick estimate that real personal consumption expenditures were up 40–58% in 1946 compared to 1939. Both economists have real consumption expenditures rising modestly thereafter.

The immediate post-war period doesn’t look like the start of a recession to me. The rapid labor-market restructuring directly contradicts Sahm’s assertion that new labor-market participants need an unusually long time to find work. (It is, after all, exactly what most immigrants come to America for.) Her silence on such an important and relevant historic episode is discrediting.

But for the sake of argument, let’s suppose Sahm’s new-entrant-delay theory is true. An important question remains: has it always been true?

If yes, then why didn’t she warn about it in her original writing?

If not, what changed between 2019 and now?

Supply & Demand

Economists love to dive into minutiae. But detailed arguments often cede too much ground.

It’s far more powerful to show someone has screwed up something fundamental or basic, like supply and demand. Unwittingly, Sahm either proves official labor statistics are unable to accurately track basic supply and demand, or that she grossly misunderstands them.

I appreciate that immigration is a hot-button issue. I raise the issue not to ruffle feathers, but to say the least controversial thing possible: immigration impacts the supply of labor and therefore labor statistics.

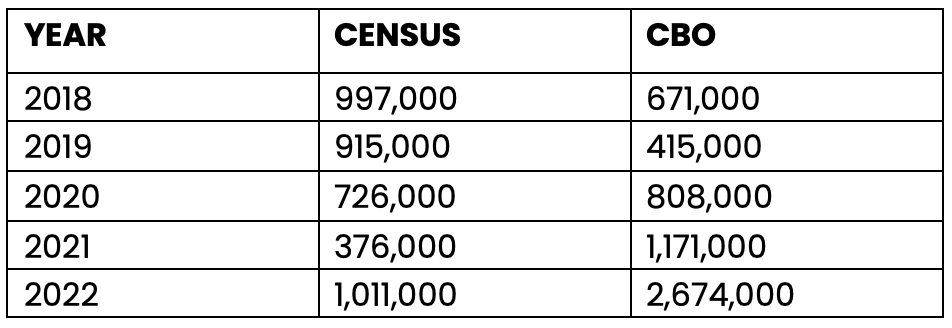

The table below shows net immigration estimates from both the US Census Bureau and the Congressional Budget Office.

Sahm credits immigrants with curing the “labor shortage” and relies on them to explain away the false positive. Immigrants were the new labor supply, prolonging an elevated unemployment rate.

But what was Sahm saying about immigration in the recent past?

From her X account on November 24, 2021:

- “Massive pull back in immigration in US is causing problems.”

February 11, 2022:

- “Immigrants have always been crucial. It’s tragic how we’re welcoming so many fewer now.”

April 11, 2022:

- “More immigrants—especially those with less credentialed education—would help address some of our most acute labor shortages… despite much of the rhetoric, immigration to the US has fallen like a rock, even before the pandemic.”

April 22, 2022:

- “For a whole host of reasons we need to welcome more immigrants to the US.”

November 15, 2022:

- “Immigration is at rock bottom.”

From a blog post dated December 14, 2022:

- “The number of immigrants has steadily fallen for years, and it plunged in 2020 when the pandemic began. The backlog of greencard applications is in the millions, including hundreds of thousands of workers.”

From her blog on February 17, 2023:

- “And immigration is moving back towards pre pandemic levels, which, with immigrants’ high labor force participation rates, should help ease the labor shortages.”

But just a few days later, she changed her tune. In a Financial Times article published February 23, 2023, she finally recognized:

- “Last year, 1mn more immigrants came to the US, continuing the rebounds from pandemic lows.”

It’s unfortunate but unsurprising that I couldn’t find a single instance of her admitting to being wrong about the direction and scale of immigration. But I want to know how she could ever be wrong in the first place.

Sahm will be the first to tell you that every 0.1 move in unemployment is critically important. This February, she posted a celebratory GIF because the unemployment rate held flat at 3.7%. Now it’s 0.5% higher, after having risen to 4.3% in the prior month’s reporting.

A change in circumstance for relatively few people can affect the statistics. Just consider what happened from July to August this year. The number of unemployed people dropped from 7,163,000 to 7,115,000 people: a mere 48,000 people and a change of just 0.7%. This coincided with the unemployment rate falling from 4.3% to 4.2%.

We’re to believe that the metrics are so finely tuned that the BLS can meaningfully track the employment status of a few thousand people. And simultaneously, they’re so porous that the supposed preeminent labor market economist underestimated, in real-time, immigration by hundreds of thousands, if not millions.

This is absurd.

Credit where due, Sahm admits to not understanding labor supply.

From her X account on August 5, 2022:

- “Yes, I know the labor participation rate is stuck so no idea where the workers are coming from but labor shortage is best solved with labor.”

It appears the mystery has been solved. But this raises an important and obvious question: If you misunderstand the supply of something, how can you accurately understand the demand for it?

818,000 Downward Job Revision

As I’m sure you’re aware, the BLS released revised jobs data, wiping out 818,000 jobs it previously claimed were created.

Sahm took to Bloomberg to dutifully defend the BLS with utterly basic points: revisions are normal and necessary; speed comes at a cost; other countries are worse and slower; etc. She insists “revisions also reflect a commitment to high-quality statistics.”

Insinuating that it couldn’t be done any sooner than August 2024, she explained away the revision as the BLS gaining access to tax records and unemployment insurance information. She failed to mention that the team at Zero Hedge, using data published by the Philadelphia Federal Reserve, warned readers of an 800,000 overstatement back in March.

But my favorite part of her commentary on the revision is not what she said, it’s what she didn’t say.

Sahm didn’t offer a single comment on the economy or labor market during the months affected by the revision. Not a word about how the revision impacts where we sit today. Her silence implies the 818,000 downward revision is immaterial.

How can such a sizable revision be so unremarkable?

Soft Landing’s Goal Posts

Sahm is on Team Soft Landing.

A MarketWatch piece dated December 10, 2022, claims Sahm expected a soft landing in 2023. Taking another bite at the apple, a Financial Times interview published December 8, 2023, quotes her as saying:

The soft landing is not here yet. But it is in the bag.

A soft landing is 2 per cent [sic] inflation or spitting distance, say under 2.5 per cent, while unemployment stays low, right around 4 per cent or below. We’ll have it next year. You can see the landing strip.

I’ve never seen anyone use the term “spitting distance” to give themselves a 25% margin of error. But hey, that’s modern economics for ya.

From her X account on February 2, 2024, we have these parameters:

- Soft Landing: inflation to 2%, unemployment low (no recession).

- Hard landing: inflation to 2%, unemployment high (recession).

- No landing: inflation stuck above 2%, unemployment low (no recession).

I have questions.

“Low” or “high” unemployment compared to what? “Stuck above 2%” by how much? What about simultaneous “sticky” inflation and “high” unemployment? Why is there no temporal element? For how long must certain benchmarks be maintained?

Call me cynical, but I suspect these aren’t oversights. A key part of the game economists play is to redefine as necessary.

In November 2023, she called “her” recession rule “highly accurate.” In February 2024, she wanted to use “recession” and “no recession” as goalposts. And in August, she cast aside “her” recession rule in a couple sentences and without reference to any scholarship, study, or empirical evidence. It was a mere assertion, simultaneously simple yet “unpredictable.”

Sahm’s February parameters are not economic criteria, they’re economic tarot cards.

Vagaries.

The setup for a parlor trick.

Pick Your Game

The Soft Landing debate will linger on. Mainstream economists will continue to position themselves so that they can claim victory regardless of what happens, and when.

But there’s no need to get distracted by their song and dance. Markets move after official statistics are published. But the buzz is extremely fleeting. Economic statistics are retrospective, whereas the markets look forward. It’s best to focus on what happens between data releases.

I probably don’t need to remind you that Lobo and I are on Team Hard Landing. But that doesn’t mean we expect an official recession call from the NBER. In fact, I’d bet against it.

We’re fond of Lyn Alden’s theory of Fiscal Dominance—the idea that fiscal policy (huge deficit spending, even when “times are good”) is more important than monetary policy today. This won’t change regardless of who’s in the White House next. If the brown stuff hits the fan, expect bailouts and stimulus checks either way. But Fiscal Dominance is not an invitation to ignore the Fed. If Powell sees trouble, his money helicopters will take flight immediately, joining those already unleashed by Congress.

They’ll flood the system with money until the statistics improve. Not that papering over the problem is a long-term solution, but the reversal from panic to party could be quick.

It’s frustrating, but there’s still no clear winner and markets are still uncertain. Seems like it’s a good time to get prepared for a variety of “landings,” so to speak.

You’re probably familiar with the case for gold. We like uranium regardless of which way the economy turns. But you don’t want to miss one of Lobo’s recent interviews where he lays out which resources he expects to take off if the worst is behind us.

KJ

P.S. There’s only one place to get Lobo’s latest thoughts on the macro picture and how it’s impacting his investments—consider subscribing to our free, no-hype, no-spam newsletter: the Speculator’s Digest.