by Konstantin Ogurchenkov

Getting into trouble is simple. Just walk into a local pub and loudly trash-talk the local sports team. Baseball, hockey, soccer… it doesn’t matter. People obsessed with their superstars will quickly help you reconsider. Fighting or running skills help in this case.

It also applies to the investment crowd. No one wants to hear that their favorite bet is about to turn around. It doesn’t matter if you make sense or turn out to be right after all. Most people don’t take criticism well. At least, most need time to digest the message.

People often listen and filter information according to what they believe. Smart ones, though, take notes. They notice when time proves who was right, and they listen better the next time.

Lobo walked into the Vancouver Resource Investment Conference (VRIC) last January, calling for a correction in uranium prices—even on the uranium panel. (In case you missed it, here’s a recording of the session, starting at a question to Lobo.)

Credit: the Jay Martin Show.

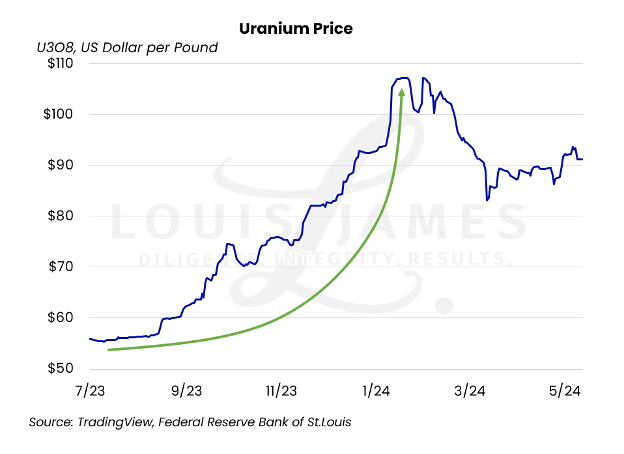

That was shortly after uranium had gone vertical—that’s what Lobo is showing with his hand above—reaching $106 per pound. It turned out to be the peak of last year’s uranium rally. It was the main reason Lobo was calling for a healthy correction—not a fall-off-the-cliff event.

No one threw rotten tomatoes, but most didn’t like his call—or want to believe him. But the Independent Speculator called it like he saw it anyway. Those who have followed him and trust his track record were prepared for the correction. Those who ignored him seemed more inclined to vent their hate on social media than learn from the episode.

The history lesson is amusing, but what’s more important is what investors should expect from uranium going forward.

Was that it? Is the price heading back to $20 per pound?

Or is the next stop the moon?

Let’s dig in.

A Healthy Correction

First and foremost, no price can surge forever.

Extreme market events can lead to a rapid rise, but it always ends with a correction.

Whether it’s war, flood, market disbalance, or some other black-swan event, prices always stop soaring at some point. They either correct and plateau if there’s been a game-changer, or they crash back down to long-term trends. Unfortunately, it’s not simple to see the end of the cycle from the top, nor which way a correction will play out.

However, investors can study the basics to get ready.

One of these is the famous adage: “No one ever went broke taking profits.”

That’s how Lobo saw uranium last January.

He didn’t know when or how much prices would correct, but the odds strongly favored some sort of correction. He was right: uranium spiked from around $50 per pound last summer to $106 in January, and has now corrected to around $90.

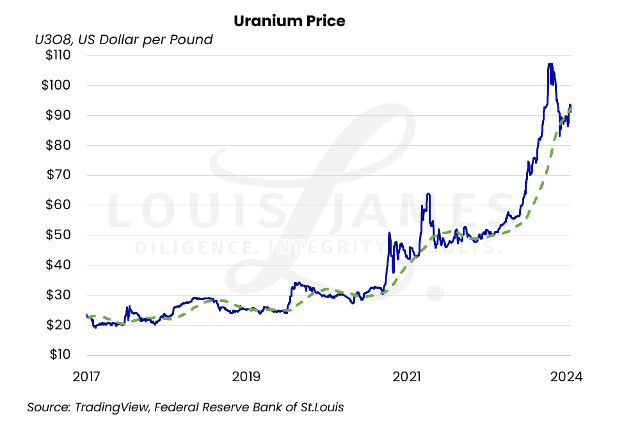

Looking at a longer time frame, we can see how the 120-day moving average (green line, below) smooths out the volatility. We’re not turning into technical analysts; the point is to show how abnormal the price action was during the recent spike.

Clearly prices surged too fast, too far, so they corrected. That’s normal—and should have been expected.

However, remember that the uranium market is small and opaque. Investors often have trouble finding daily prices and often see lagging trading effects.

Other commodities, such as copper, oil, wheat, cocoa, etc., have much more transparent pricing data, which allows investors to make more well-informed decisions.

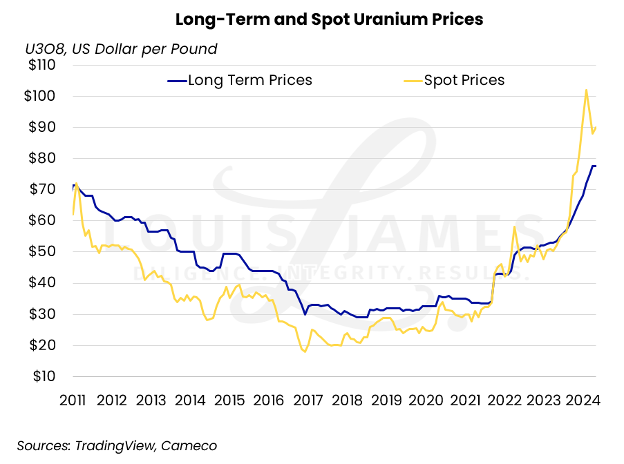

Also, the uranium price charted above is the “spot” or short-term price. It’s only one of the pricing tools investors have in their toolbox. A more accurate picture comes from long-term contract prices. These are the prices nuclear utilities use to secure supply for their long-term contracts.

Here’s how long-term prices compare to spot prices.

As you can see, the two are closely related. However, spot prices are usually lower than long-term ones. In fact, during the 2007 surge, these lines parted for only a couple months. Then the spot price came back to its long-term counterpart.

We’re seeing the same thing now. The spot went over the long-term price and was due for correction.

What’s critical now is that long-term prices are rising.

If it weren’t so, spot would have a painful bear trend ahead, trashing share prices in uranium companies as it went.

The rising long-term price is a strong vote of confidence for uranium bulls, in addition to the very fundamentals, which still point to its shortage (see our free uranium report for an in-depth look at this).

Risks

A Chernobyl-scale event would derail the current nuclear renaissance. This is extremely unlikely, given many advancements and new, safer technologies, but it’s a risk all investors in this space should be aware of.

A greater risk would be too-rapid expansion of existing mines or restarts of idle operations. This could flood the market with new supply faster than the growing demand can meet.

Indeed, the cure for high prices is high prices; this will eventually happen.

But we don’t expect it in the next several years, leaving us with plenty of time to profit.

Less likely, but possible, is that anti-nuclear activism could block and disrupt the demand side of the equation. There will always be some opposition—heck, the coal sector might even fund them.

Our view is that climate-change panic is so intense, nuclear energy will come out ahead.

Takeaways

It takes guts to admit that your top investment is about to correct in price. But it’s better to be aware of such a possibility and prepare for it.

We saw a correction in the uranium price as necessary and to some extent, healthy. The fact that the price didn’t collapse to below the cost of production tells us that demand is solid enough to keep the price from falling off the cliff.

Never say never, but a complete crash in uranium prices is unlikely, especially given the limited supply and growing demand.

It’s also important that uranium miners sign long-term contracts now at or near triple-digit prices. The more spot prices drop, the greater their incentive to buy on the spot market to meet their contractual obligations without depleting their own reserves in the ground. This is why long-term contracts are so important.

We maintain our bullish outlook on uranium prices. But even if they “stagnate” at current levels (around $90), that’s enough for most miners to post profits. The better ones gush cash at these levels. That should deliver wins for shareholders, regardless.

Investors still have a chance to benefit from the current pullback and invest in high-quality uranium names. With proper stock selection, the gains could be exceptional.

As Lobo says…

Caveat emptor,

KO

P.S. If you’d like help picking better uranium (or other resource) stocks, My Take could be just the thing for you.